To possess members having a current Laurel Path student loan:

October 3, 2024Understanding Primobolan Oral Administration

October 3, 2024Personal mortgage insurance (PMI) try an insurance plan that handles the lender if you default toward paying off the mortgage. They discusses most of the otherwise a fraction of your leftover home loan balance, and it is sometimes expected.

Definition and you will Example of Individual Financial Insurance

Private mortgage insurance rates could have been an element of some home loans just like the 1957. It efficiently claims the financial institution one the financing would be reduced, very that have eg an insurance policy in place can help specific consumers become approved for a loan they won’t or even qualify for. That it insurance is often required if one makes a down-payment off lower than 20%.

- Acronym: PMI

Some loan providers makes it possible to build a down payment out-of below 20% without paying getting PMI, nevertheless these funds constantly feature steeper rates of interest.

Exactly how Private Home loan Insurance coverage Work

Like most different kind of insurance policy, you are purchasing premiums to fund problems is always to an unfortunate experiences can be found. The insurance business is liable for paying down the loan in the event the for some reason you find yourself struggling to do so.

Lenders thought that this is much more browsing occurs if you have less of a possession risk throughout the possessions. This could be possible when your equity were lower than 20% at the outset since you didn’t put the far money off.

Personal Financial Insurance versus. Financial Defense Insurance coverage

PMI differs from financial shelter insurance (MPI). Mortgage shelter insurance would not pay-off the entire harmony of your own loan for individuals who standard, nevertheless could make particular money to you personally for a while for those who slip prey to particular covered hardships, including jobs losings, impairment, otherwise serious illness.

Pros and cons from Individual Mortgage Insurance coverage

You’ll find both advantages and disadvantages so you’re able to PMI. On upside, it generates they easier to be eligible for that loan, since it reduces the chance your present to a loan provider. They are even more prepared to overlook the lowest credit rating or faster down-payment. And you will premiums is actually tax deductible, at the very least as a result of tax season 2021. This has been those types of previously-altering areas of tax rules that change from 12 months to seasons.

PMI plus offers alot more to order power. It reduces the downpayment you will be required to give the fresh new table, and is very useful if you find yourself brief on funds or just want a lower life expectancy very first money.

Area of the downside out of PMI is the fact it does increase their month-to-month mortgage repayment. It can possibly improve closing costs, also. Another disadvantage is that home loan insurance rates can be found only to guard the new bank in case you default. It’s got no safety to you personally after all if you fall behind to the costs.

Carry out I want to Pay money for Personal Financial Insurance?

To prevent PMI typically need and work out a down payment out of 20% or more. That isn’t real of all lenders, however it is a good principle.

These insurance policies usually costs anywhere between 0.5% and you may step one% of loan worth to the a yearly basis, nevertheless the price of PMI may differ. The financial often detail the PMI superior in your 1st mortgage guess, and on one last closure disclosure form. You will definitely shell out your own superior either initial in the closing, monthly as an element of your own mortgage repayments, otherwise one another.

The good thing about PMI is that it is really not permanent. You could potentially generally speaking demand your PMI getting canceled and removed from your own mortgage payments when you’ve gathered 20% security of your property. The process for it may differ of the bank, although request must always have writing. It have a tendency to needs some other assessment of your property.

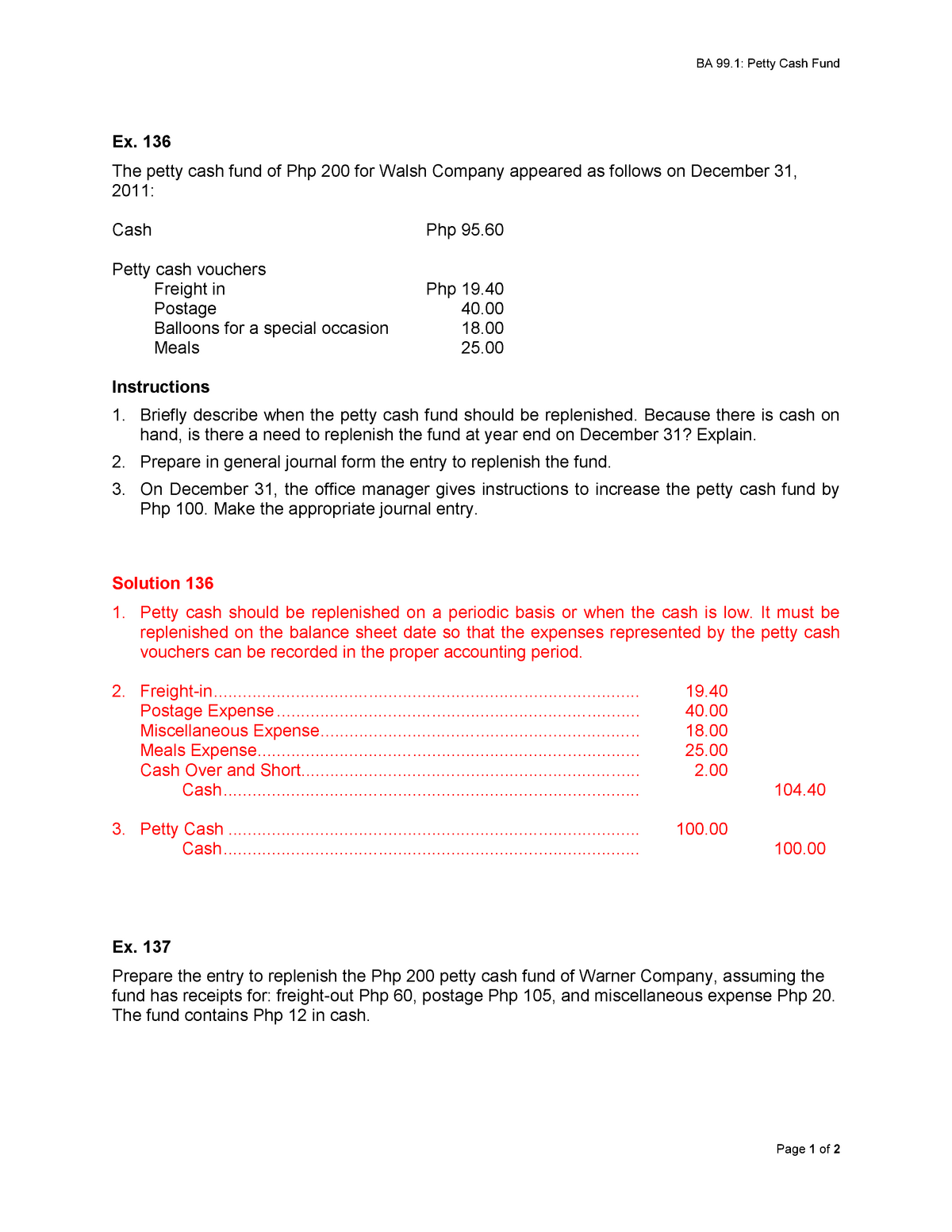

Get in touch with the lender since you nearby the 20% I. Your own lender is required to cancel PMI online loans Margaret Alabama for you after your debts drops in order to 78% of your own home’s well worth, however you must be most recent on your money ahead of capable terminate your own policy.